Alex Morris is the founder of TSOH Investment Research Service. Prior to launching his company, he worked as a buy-side equities analyst for 10 years.

What’s the big idea?

In 2018, Berkshire Hathaway publicly released video recordings of their shareholder meetings, dating back to 1994. Covering a total of roughly 150 hours and more than 1,700 questions, the content of these meetings presents a rare collection of investment and business wisdom.

Below, Alex shares five key insights from his new book, Buffett and Munger Unscripted: Three Decades of Investment and Business Insights from the Berkshire Hathaway Shareholder Meetings. Listen to the audio version—read by Alex himself—in the Next Big Idea App.

1. The role of continual learning and a willingness to change.

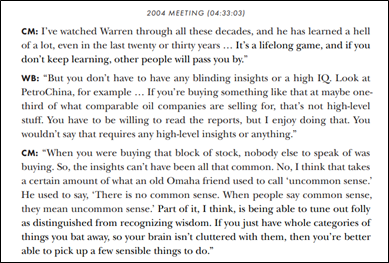

Warren Buffett’s early years in the investment business consisted of cigar butt investing—finding a soggy cigar on the floor, with only one free puff left. That largely consisted of investing in companies where the net assets on the balance sheet more than covered the cost of the business in the stock market. It relied on the value of tangible assets, which could be quantified and valued with a certain level of specificity. Buffett’s approach evolved to recognize the value of intangible assets as well, most notably with the See’s Candies acquisition in 1972. As Munger recounted at the 2004 meeting, continual learning and refinement of his approach was a key factor in Buffett’s long-term success:

2. The importance of proper incentive structures.

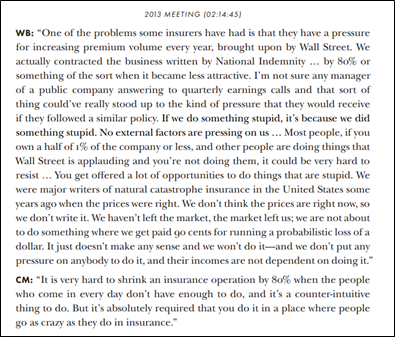

As investors and managers, Buffett and Munger have witnessed how incentives drive behavior. In some notable instances, like the Wells Fargo fake account scandal in the mid 2010’s, companies Berkshire was invested in were negatively impacted by the deleterious impact of faulty incentive structures. Inside Berkshire, one business that has been greatly impacted by incentives is insurance operations.

As Buffett and Munger discussed at the 2016 meeting, the pressures that arise for public companies, most notably in terms of delivering short-term results that satisfy stock market investors, must be fully considered; otherwise, the tail will wag the dog, and short-term incentives will outweigh intelligent long-term decision-making.

CM: “The main thing is practically nobody else does it. And yet, to me, it’s obvious it’s the way to go. There’s a lot in Berkshire like that. It’s a little different from the way other people do it; it’s partly the luxury of having a controlling shareholder of strong opinions… It would be hard for a committee to come up with these decisions.”

3. Focus on what’s important and knowable.

A recurring theme at the annual meetings were shareholder questions about big unknowns—think macroeconomic developments, geopolitical concerns, etc. When pressed on these topics, Buffett and Munger often returned to two straightforward ideas: think long-term and less is more. At the 1998 meeting, Buffett presented a historic example that helped frame why narrowing one’s purview can be a superpower in investing.

4. The risk of false precision.

A key part of long-term investing is to be roughly right about the key variables instead of being precisely wrong due to overconfidence and an insufficient margin of safety. A prominent example in finance is the Efficient Market Hypothesis and the Capital Asset Pricing Model. These were widely taught approaches at higher universities in the 1980’s and 1990’s for thinking about markets and measuring risk. As Buffett and Munger discussed at the 1998 meeting, the academics had overdosed on mathematics; their quest for precision led them astray.

5. When possible, avoid difficult decisions.

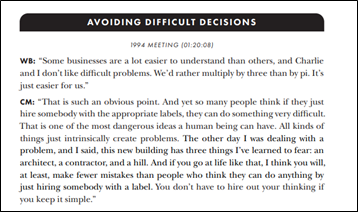

When Charlie Munger reviewed a potential investment, he’d put it into one of three piles: in, out, or too hard. In investing, there are no called strikes; you can patiently wait with the bat on your shoulders for a great pitch to swing at. This idea is applicable in other parts of life as well. As Buffett and Munger discussed at the 1994 shareholder meeting, the things they’ve avoided were a key part of how they succeeded in picking among what was left over.

To listen to the audio version read by author Alex Morris, download the Next Big Idea App today: